Are you looking to improve your credit score in Ontario? Having a good credit score is essential. You need it whether you’re looking to buy a home, get a loan, or improve your financial standing. In this comprehensive guide, we’ll explore the basics of credit scores. We’ll also cover common mistakes to avoid. We’ll discuss effective DIY credit repair strategies. We’ll also explore when to consider using professional credit repair services in Ontario. We’ll also provide more resources to help you on your journey to credit score improvement.

Credit Score Basics: Understanding What Affects Your Credit Score

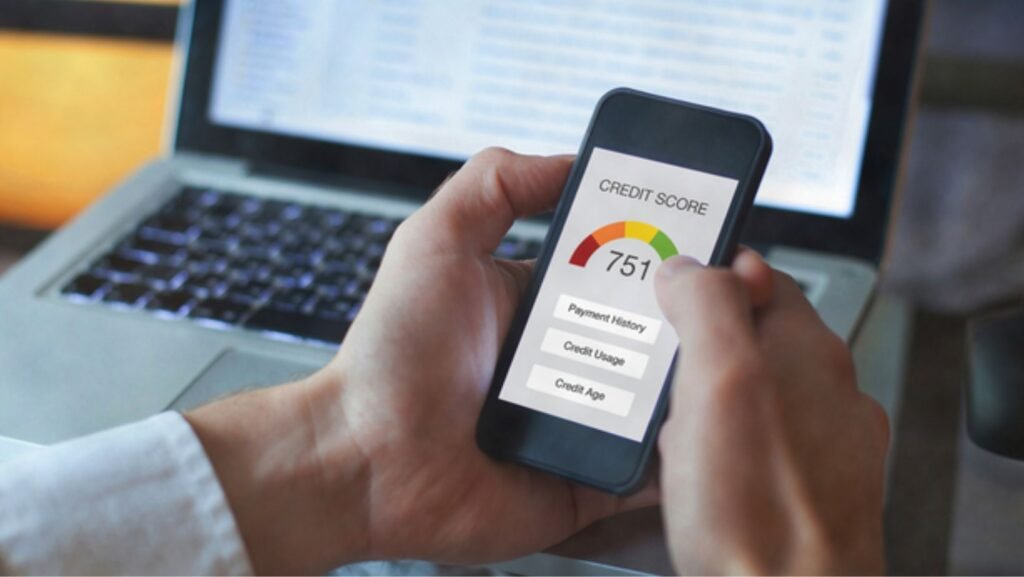

Credit scores are crucial for personal finance. They impact an individual’s ability to secure loans, mortgages, and even employment opportunities. You need to understand the factors affecting your credit score. This is essential for taking control of your financial well-being.

Your payment history holds the most significant weight in determining your credit score. making on-time and complete payments demonstrates your reliability as a borrower. late payments or defaults can have a detrimental impact on your score.

Credit use, or the amount of credit you’re using compared to your credit limit, also plays a vital role. Maintaining a low credit use ratio indicates responsible credit management. Maxing out your credit cards can affect your score.

The length of your credit history is another important factor. Lenders have more data to assess your creditworthiness if you have a longer credit history. A lengthy history of responsible credit management can boost your score.

Diversify your credit portfolio. Have a mix of different types of credit, such as credit cards, installment loans, and mortgages. This can also impact your credit score. This demonstrates your ability to handle various forms of credit .

Finally, be cautious when applying for new credit. Applying for many credit accounts in a short span can raise concerns about your financial stability and lower your credit score. Only apply for credit when necessary and avoid unnecessary inquiries.

By understanding these key factors, and adopting responsible credit habits, you can improve your credit score. This can unlock better financial opportunities.

Common Credit Score Mistakes To Avoid in Ontario

When striving for a Credit Score Improvement Ontario, it’s crucial to avoid common pitfalls. These pitfalls could set you back. Being aware of these potential missteps can safeguard your credit score and prevent unnecessary damage. It can pave the way for steady improvement.

One of the most detrimental mistakes is making late payments or, even worse, missing them . Payment history carries significant weight in determining your credit score. Providing timely payments is of utmost importance. Even one instance of tardiness can have a negative impact. This underscores the importance of diligent financial management.

Another common pitfall is overextending yourself by maxing out your credit cards. Exceeding your credit limit or maintaining a high credit use ratio can lower your credit score. Aim to maintain a low credit usage ratio, below 30%, to prove responsible credit management.

Applying for too much credit at once can also disrupt your credit score progress. Each time you apply for a new credit account, the lender makes a hard inquiry on your credit report. This can lower your score. Avoid submitting many credit applications within a short period unless necessary.

Closing old credit accounts is another mistake to avoid. The length of your credit history influences your credit score. It’s beneficial to keep older accounts open, even if they’re not used. Closing older accounts can shorten your credit history andlower your score.

Finally, failing to use credit can hinder your credit score improvement efforts. This includes neglecting to make payments on time, exceeding your credit limits, and failing to use your credit accounts. Responsible credit usage demonstrates your ability to manage credit. It also contributes to a higher credit score.

Avoid these common credit score mistakes in Ontario. Taking charge of your financial well-being, work towards achieving a higher credit score. Remember, credit score improvement is gradual. Consistent effort and responsible financial habits are the keys to unlocking your credit score goals.

DIY Credit Score Improvement Ontario: Proven Strategies For Success

In this section, we will provide you with proven DIY credit repair strategies. They can help you improve your credit score in Ontario. These strategies include disputing errors on your credit report. Your credit report may have incorrect or old information. This could affect your credit score. By disputing these errors with the credit bureaus, you can have them corrected. This can improve your score.

Paying your bills on time and in full: This is one of the most important things you can do to improve your credit score. Late and missed payments can hurt your credit. Making on-time and complete payments shows your reliability as a borrower. Keep your credit use ratio low. Credit usage refers to how much credit you are using compared to your credit limit. Aim to keep this ratio below 30% to show lenders that you are not overextending yourself. Getting a credit builder loan is a type of loan designed to help you build or Improve Your Credit. You will make monthly payments on the loan, and as you make payments on time, your credit score will improve.

Becoming an authorized user on someone else’s credit card: If you have someone in your life with good credit, you may be able to become an authorized user on their credit card. This can help you build your credit history and improve your credit score.

By following these strategies, you can take control of your credit score. This will help improve your financial well-being.

Professional Credit Repair Services in Ontario: When To Consider Them

Professional credit repair services can be a valuable resource for individuals facing complex credit challenges. Here are a few instances when you should consider professional credit repair services. This may be advisable.

- Severe Credit Problems: Professional credit repair services can provide specialized expertise and strategies to address low credit scores and derogatory marks, like bankruptcies, foreclosures, or judgments, on your credit report.

- Complex Credit Issues: Dealing with complex credit issues, such as identity theft, credit report inaccuracies, or disputes with creditors, can be time-consuming and challenging to resolve on your own. Professional credit repair services use their experience and knowledge to navigate these complexities and ensure the protection of your rights.

- Time Constraints: If you lack the time or resources to dedicate to credit repair, professional services can ease this burden. They can handle time-consuming tasks. This includes reviewing credit reports, disputing errors, and negotiating with creditors. This allows you to focus on other important aspects of your life.

- Lack of Comfort with Credit Repair: If you feel overwhelmed or uncomfortable handling credit repair on your own, professional services can provide peace of mind and guidance. They can explain the process, answer your questions, and ensure that you are making informed decisions about your credit.

Before engaging a Professional Credit Repair Service, research and choose a reputable company with a proven track record and positive customer reviews. Make sure they are transparent about their fees and services. Avoid companies that make unrealistic promises or charge upfront fees. Additionally, prepare to provide accurate information and documentation to support your credit repair efforts.

More Resources For Credit Score Improvement in Ontario

This section provides more resources for credit score improvement in Ontario. These resources include government agencies, credit bureaus, and non-profit organizations. They offer credit counseling and education services.

Equifax and TransUnion are two of the major credit bureaus in Canada. These bureaus collect and maintain credit information on consumers. They also provide credit scores to lenders. You can get a copy of your credit report from Equifax and TransUnion. This allows you to review your credit history. You can identify any errors or discrepancies.

Several non-profit organizations in Ontario offer credit counseling and education services. These organizations can provide personalized advice. They can also help you develop a plan to improve your credit score. Some reputable organizations include the Credit Counseling Society of Canada. Consolidated Credit Counselling Services of Canada is another option. Money Mentors is also reputable.

Using these resources can help you understand your credit score. They can also help you identify areas for improvement. Then, they can help you develop strategies to repair and improve your credit. Remember, improving your credit score takes time and effort. But, it is achievable with consistent effort and responsible credit management.